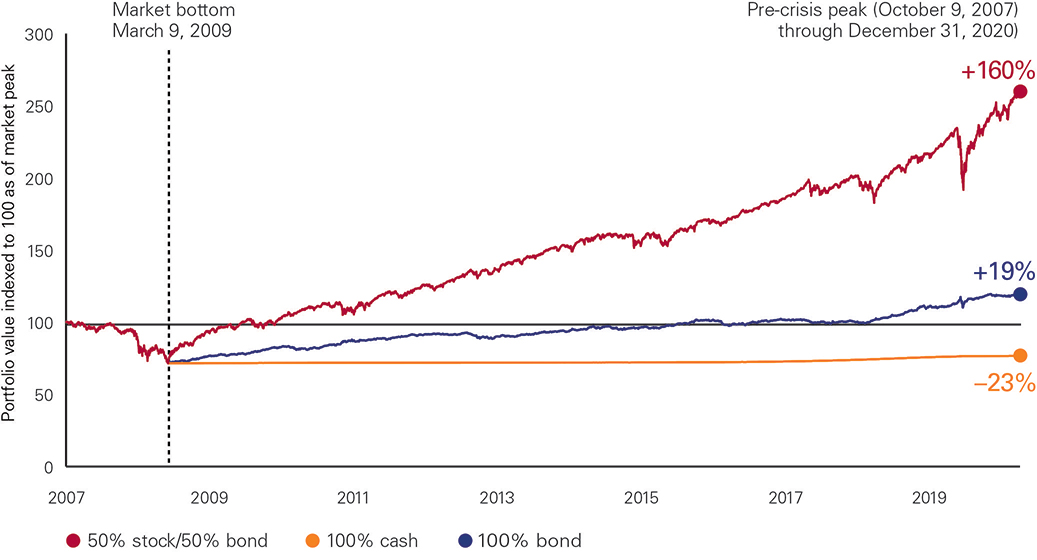

Changing your investment mix can backfire. Consider three hypothetical investors, who took three different paths. As shown in the chart below, each had a 50% stock/50% bond portfolio during the downturn that ended in March 2009. One held tight and maintained the same portfolio, recouping the unrecognized losses in about a year and a half and enjoying the subsequent rebound in stocks. The other two radically revamped their portfolios, one moving all to bonds and the other all to cash. Roughly ten years later, both of the latter portfolios continued to suffer the consequences, with their values remaining below their peaks.

Source: FactSet.

Notes: The 50% stock/50% bond portfolio is represented by the Standard & Poor’s 500 Index and the Bloomberg Barclays U.S. Aggregate Bond Index (rebalanced monthly). The 100% bond portfolio is represented by the Bloomberg Barclays U.S. Aggregate Bond Index. The 100% cash portfolio is represented by 3-month Treasury bills. This is a hypothetical illustration.

The final account balance does not reflect any taxes or penalties that may be due upon distribution. Withdrawals from a traditional IRA before age 59½ are subject to a 10% federal penalty tax unless an exception applies.

Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

All investments are subject to risk, including the possible loss of the money you invest.

The Bottom Line:

Emotions and investing can be a losing combination. Don’t abandon your investment mix just because the market is uncertain.